Argentina’s economic situation and outlook

The libertarian government has reduced inflation from almost 250% in November 2023 down to 33% now. It’s still a very high rate -almost ten times the inflation rate of a decent country- yet it is a formidable achievement for a singular case like Argentina.

Argentina is a singular country for many reasons you must know:

1. Back in 1974, half a century ago, income per capita was 60% of average income of advanced countries.

2. People living in poverty were 4% of population. Nowadays they are more than 30%, and when inflation spikes the figure reaches 50%.

3. In the years between then and 2023, the country experienced true hyperinflation, true banking panic, and almost radical populism, besides authoritarian rule and two wars, one internal (against insurgency) and the other external (against the UK).

4. I say true hyperinflation because it was no less rapid than classic hyperinflations of the 1920s in Austria, Hungary, and Poland. I say true banking panic because it was as dramatic, though shorter, than the American panic of the 1930s. I say almost radical populism because it was almost as aggressive and only less long than in Venezuela.

To get inflation down, the incoming government did two things at once:

a) devalue the peso 27% in the (official) foreign exchange market in January 2024 and 2% monthly up to next December;

b) freeze national public spending in nominal terms for as long as necessary.

What happened next?

* Public spending fell 24% in real terms in 2024. The government allowed only meager wage increases and cut sharply investment spending as well as grants to provinces.

* The Central Bank bought 20 billion dollars in the forex market.

Why?

The peso devaluation through 2024 resulted in even higher inflation. And inflation did the dirty work: it reduced real spending and produced an excess demand for pesos and its equivalent excess supply of dollars in the forex market, which the Central Bank readily bought by money printing.

In this fashion, two goals were achieved: i) the government went from a primary fiscal deficit about 5% of GDP to a surplus about 1%; ii) the government also got funds to meet capital services on the national debt.

Yet the financial problem was much bigger and more dangerous than that.

I have in mind the quasi-fiscal deficit; that’s the interest payments on the Central-Bank peso debt. In 2023, as it occurred many times in the last 70 years, the government run a very large deficit, printed a lot of money to cover it, and -to lessen its impact upon inflation- the Central Bank placed peso debt with commercial banks. This debt is known as non-monetary liabilities (NML) of the Central Bank, and interest payments on NML are known as the quasi-fiscal deficit. That is how a dangerous situation was created.

* NML were 2,5 times the monetary base. Then if banks took the decision not to hold NML anymore, the price level might jump 250% at once, undermining the political stability of the government.

* Interest payments on NML were endogenous, meaning they were not controlled by the government. For them to be held by the banks, the Central Bank must pay the American interest rate plus the expected rate of peso devaluation in the official forex market, a rate that depends on market expectations. So that the trajectory of this rate becomes crucially important. If it converges on the actual rate of peso devaluation, NML stock would fall and interest payments would be manageable. If not, there would follow a sharp run up in the forex market and an inflationary spike.

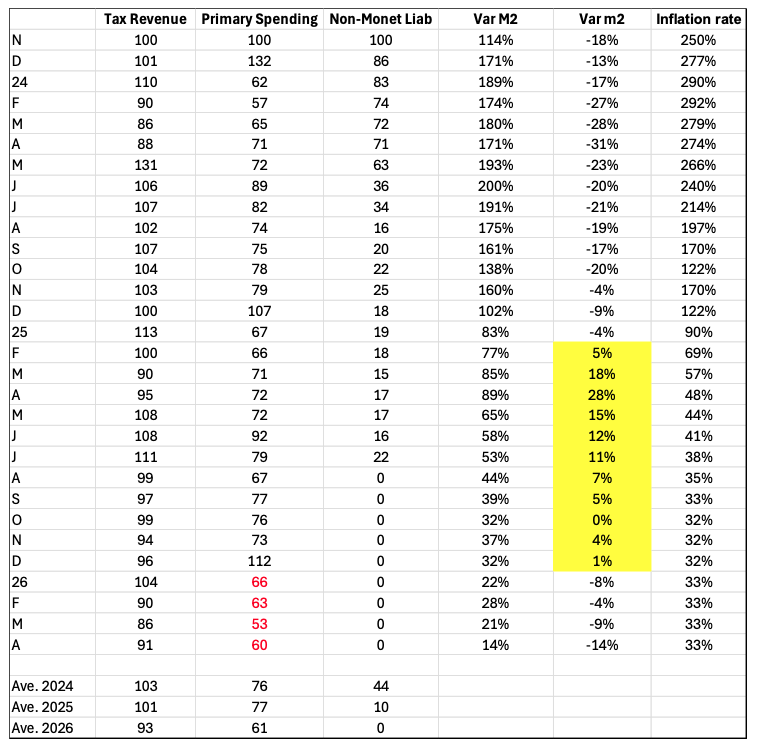

Table #1

Why all the fuss?

Because the Central Bank didn’t have enough international reserves to intervene decisively in the forex market. Everything could have gone wrong in 2024. As it happened one year later when Argentina was at the brink of disaster because of lack of reserves. Anyway, the market bought the announcement. It was a kind of miracle. By December 2024, the real value of NML was 82% less than in November 2023.

In sum, thanks to clarity of thought, resolution, and technical skill the libertarian government’s stabilization plan has been successful so far. (Primary spending in real terms kept low throughout electoral year 2025, and the real value of NML continued to fall toward zero even so the Treasury has got in debt with the Central Bank for lesser amounts.)

Finally, let’s focus on Table #1. See that, for low levels of inflation, as from mid-2025 on, the rate of inflation becomes essentially the difference between the rates of monetary growth and money demand growth. For instance, when the second is positive, inflation is lower than monetary growth, and when it is negative, inflation is higher. This observation allows me to predict that when monetary growth settles in the low single digits, inflation might drop to about zero.

Why does the government keep augmenting the money supply? Because the bond holders and the IMF want the government to print money and build up reserves to make sure it will meet its obligations.

(Speech given to foreign visitors at a Friedman-Hayek conference, Universidad del CEMA, March 2026. Data has been updated.)

Jorge C. Ávila

Profesor e investigador full time, director del CEA, Ucema.